The onset of COVID-19 pandemic in March 2020 set off a wave of domestic migration that reoriented housing markets across the country, turning some metro areas into boomtowns and sinking a number of others.

The prevailing narrative around this phenomenon took on a life of its own — a mass exodus from urban cities in coastal markets and a flight to suburban sprawls where housing was cheap and space was plentiful.

The phrase “flight to the suburbs” came to define this trend in a way that suggested that big cities were on fire and residents were running for their lives. But five years after it started, data suggests that the reality was much less dramatic and largely temporary.

There was definitely a real shift in the early part of the pandemic, but now that we are several years out, the pattern has become more complex,” said Nadia Evangelou, a senior economist with the National Association of Realtors (NAR).

“It’s not just about suburbs anymore. People are reevaluating what they want out of the community, and that’s why we’re seeing migration to certain places.”

Escape from New York (and San Francisco)

Back in 2020, Americans watched in horror at the scenes of New York City on the news — an empty Times Square, Central Park packed with make-shift morgues and Big Apple residents trapped in small apartments under a hard lockdown.

An outflow of residents began, primarily from Manhattan, where people have the means to pick up and move on a dime. Rents on the island went into free fall as apartment vacancies piled up. Year-over-year migration shows a clear shift of people leaving the city and people going to the suburbs on Long Island.

Net migration in Manhattan fell by a shocking 252% year over year in 2021, according to U.S. Census Bureau data. The boroughs of Brooklyn (-107%), Queens (-62%) and the Bronx (-50%) also dropped substantially, while the Long Island counties of Suffolk and Nassau counties saw migration gains of 235% and 71%, respectively.

But when lockdowns eased and there were things to do in the Big Apple again, these people came right back. Apartment vacancy rates went from historic highs to historic lows in a flash, and rents in the city are now substantially higher compared to the start of 2020. Conversely, the net migration inflow to Long Island flipped to a net outflow.

A similar but more muted dynamic happened in San Francisco. Wealthy tech workers left after the onset of the pandemic as more companies allowed remote work, but they’ve slowly come back, particularly as those firms have called workers back to the office.

Migration wave slowly builds, but not all at once

While many in New York and San Francisco left the city in short order, it happened more incrementally in the rest of the country.

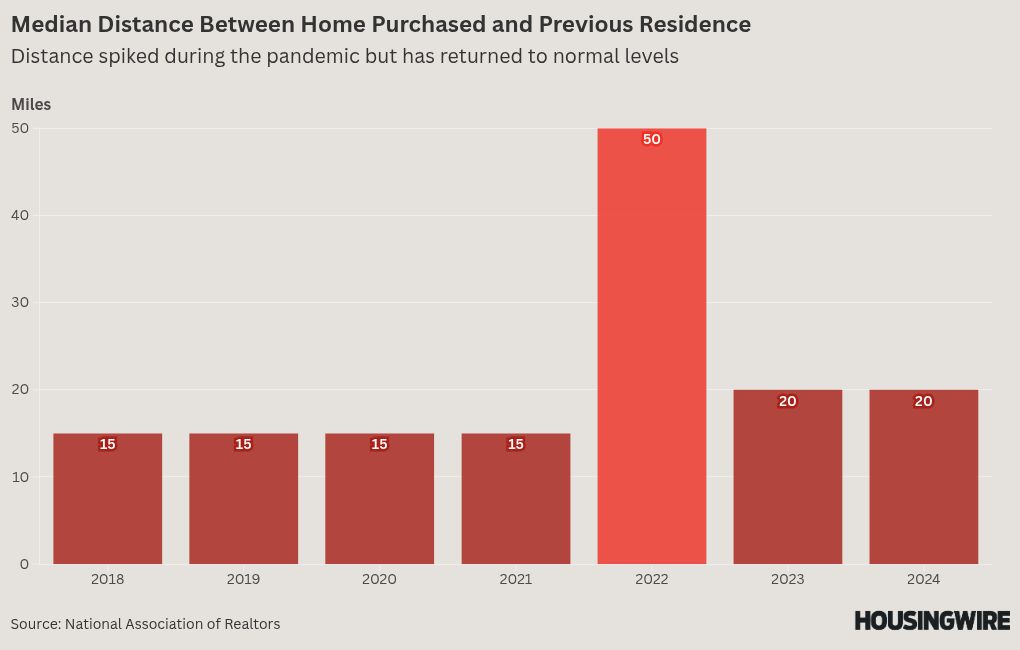

NAR data shows that the median distance for homebuyers between moves was consistently at 15 miles before spiking to 50 in 2022. In the following two years, it dropped back to 20 miles.

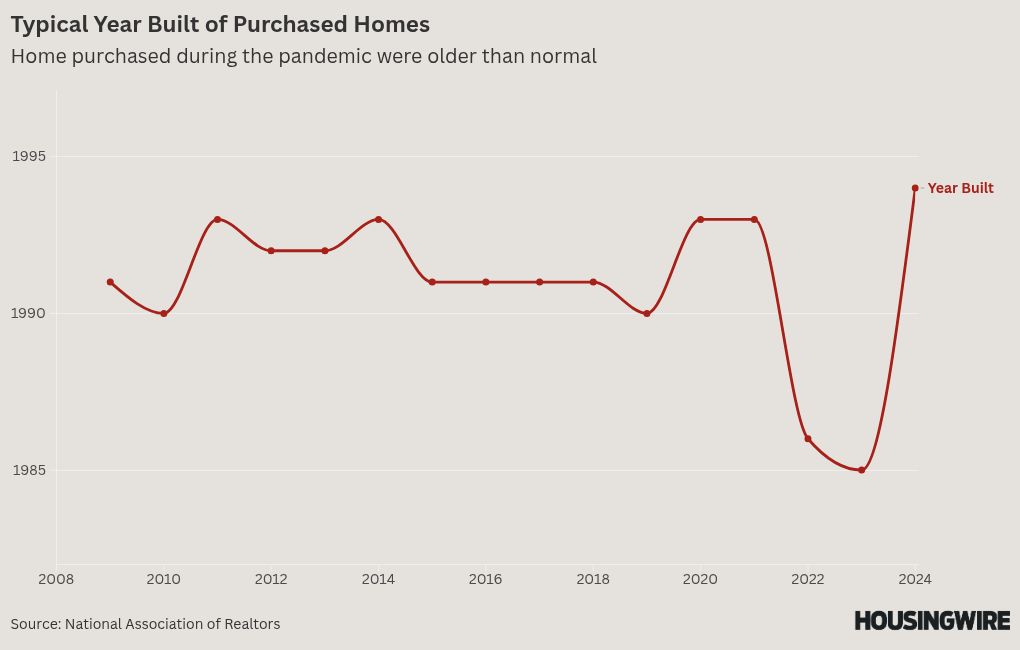

Additionally, homes purchased prior to the pandemic were usually built sometime in the early 1990s. In 2022, this plummeted to the mid-1980s, but it has since spiked back to the mid-1990s. This suggests a deviation between existing-home sales and new-home sales.

In the heat of the frenzy, existing homes were what buyers could find, which pushed up the age of homes purchased. Since then, new homes have been a bright spot in an otherwise cold market, lowering the age of homes purchased below pre-pandemic norms.

Flight to suburbs or flight to exurbs

The desire for more space was largely credited for the explosion in migration. People working from home wanted a home office, and kids learning remotely needed to be somewhere they wouldn’t be a distraction for their parents.

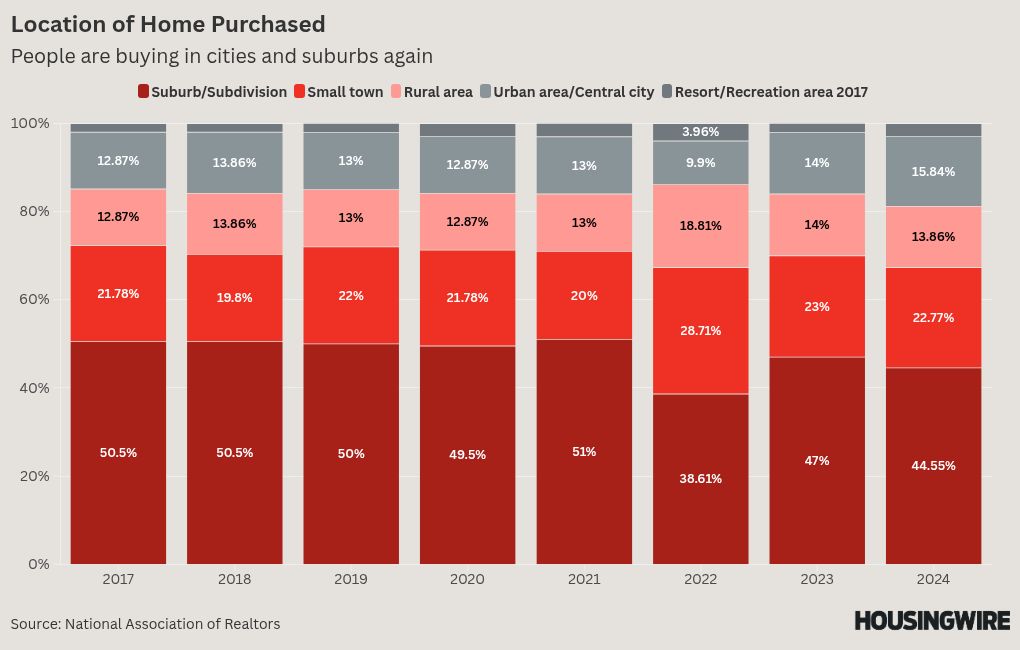

But NAR data also suggests that movers weren’t coming from urban centers to the suburbs — it was people going to the exurbs from the suburbs.

The share of home purchases in suburbs remained remarkably consistent from 2017 to 2022 at about 50%. But in 2022, that number dropped to 38%, gobbled up by purchases in small towns and rural areas. In 2024, the suburban share of home purchases remained somewhat deflated at 44.5%, with the urban share of purchases rising to 16%.

“These [pandemic homebuyers] felt like not young people who had been living the single life in the city, but rather the people doing virtual school and working from home moving up to a bigger family house with more space in the further-out jurisdictions,” said Lisa Sturtevant, chief economist for Bright MLS, which covers the Mid-Atlantic region.

A caveat is that urban centers tend to have lower homeownership rates — and that’s certainly true in New York City, where about 70% of residents are renters. Data on home purchases doesn’t pick up movement among renters, but it’s clear that their destinations weren’t necessarily the suburbs.

Pandemic housing trends weren’t new, just supercharged

Young families that are about to have a second or third child always want to buy a bigger house. College graduates who move to the city often leave when they decide to start a family. And migration to more affordable areas like Florida, Texas and the Southwest had been happening well before COVID-19.

What the pandemic did was speed up this process. Urbanites who planned on moving in two years decided to do so early given there wasn’t anything to do in the city anyway.

Another element that got lost in the narrative at the time was the impact of rock-bottom mortgage rates. A young family might not have been planning to have another child for another few years, but why not take advantage of a 3% rate while you can, especially if it results in a bigger house or a lower monthly payment?

Another understated dynamic was housing affordability, which largely drives preferences for movers. Part of why Florida and Texas are appealing to coastal residents is that they can get more bang for their buck.

“During the pandemic, we found that suburban housing markets did not generally outpace urban areas in terms of growth, with the notable exceptions of New York and San Francisco,” Zillow senior economist Orphe Divounguy told HousingWire in an email.

Hotspots turn to deep freezes

Home-price growth in some areas rose at alarming and unsustainable rates during the heat of the pandemic migration wave. A prime example is Austin, which received a huge influx of tech workers who pushed up home prices.

According to Altos data, the median home price in Austin rose by a shocking 44.8% year over year in June 2021. Miami (+18.4%), Phoenix (+27.6%), Boise (+32.8%) and Dallas (+10.1%) were not far behind.

But by June 2023, year-over-year prices turned negative in Austin (-11.6%), Phoenix (-2.8%) and Boise (-2.7%). In June 2025, each of these markets except for Boise experienced an annual decline.

This is in stark contrast to the pandemic-era cold spots. According to the S&P CoreLogic Case-Shiller Home Price Index for March 2025, New York City had the highest year-over-year price gain in the country at 8%.

Other urban cities were also seeing substantial gains, including Chicago (+6.5%), Detroit (+5.8%), Boston (+4.7%), Los Angeles (+4.1%) and Washington, D.C. (+4.5%).

With San Francisco’s reliance on tech workers who are more likely to have been granted permanent work-from-home status, its home prices have been slower to recover than New York’s but are still up 1.6% annually.

There are caveats to this. The rapid rises in home prices, inflation and mortgage rates have made affordability a sudden problem in these areas. In Florida and Texas specifically, home insurance issues have become acute.

And many companies have called workers back to the office, which limits people’s options for where to move — even if they can afford to.

“We’re certainly seeing how [pandemic hotspots] have slowed down dramatically,” said Michael Neal, a senior fellow at the Urban Institute‘s Housing Policy Finance Center. “It’s a reversal in some of those dynamics, and affordability issues have really ramped up.”